In this series about community development lending, we aim to shed light on the diverse types of loans we offer, in the hope that it will provide the clarity our borrowers need to make an informed decision about applying for a community development loan.

In this sixth installment, we explain what New Market Tax Credit (NMTC) Qualified Low Income Community Investment (QLICI) loans and how they are pivotal in supporting projects that uplift communities living with low income by providing crucial financing under favorable terms.

Understanding the New Market Tax Credit Program

The New Markets Tax Credit (NMTC) program is a federal initiative designed to stimulate investment and economic growth in urban and rural communities living with low incomes, communities that often lack adequate access to capital. The primary goal of the NMTC program is to encourage economic development and job creation in communities that are economically distressed. This is achieved by providing tax incentives to investors.

Under this program, Community Development Entities (CDEs) like Capital Impact Partners provide subsidized financing for qualifying businesses or real estate projects that meet the federal definition of a Qualified Active Low-Income Community Business (QALICB).

A QALICB is typically a business that is located in, or provides services to, communities living with low incomes. The capital provided to these qualifying projects is known as a Qualified Low-Income Community Investment (QLICI), which is typically structured as a seven-year, interest-only loan.

Understanding QLICI Loans

A QLICI is a specific type of investment that is central to the New Markets Tax Credit program. It involves directing financial capital into projects or businesses in communities living with low incomes that meet the qualifications set under the NMTC program.

A QLICI is essentially the financial vehicle through which capital flows from CDEs to QALICBs at favorable rates and terms that traditional financing might not offer.

Why is QLICI Valuable to Developers?

Access to Favorable Financing

QLICIs often come with more favorable terms than those available through conventional financial products. This can include lower interest rates, longer amortization periods, and interest-only payment periods. Such terms can significantly reduce the cost of capital for developers, making projects more financially viable.

Filling Funding Gaps

Many projects in areas experiencing low incomes struggle to secure funding because they are perceived as higher risk. QLICIs can provide the essential capital needed to fill these funding gaps and make such projects feasible. This is particularly important for large-scale developments that can have transformative impacts on their communities.

The importance of this type of loan can be seen through two QLICI notes totaling $7.7 million that Capital Impact provided for Coastal Bank Food Bank in Corpus Christi, Texas. This funding was essential for constructing a new 108,200-square-foot warehouse and distribution center. The project addressed urgent facility needs sparked by explosive growth at the food bank and was critical in a community prone to hurricanes, requiring more expensive construction to meet specific safety standards. New Markets Tax Credits played an indispensable role in the capital stack, preventing potential reductions in food distributions that would have created significant community hardship.

Enabling Comprehensive Development Projects

Developers using QLICIs can undertake comprehensive projects that might include various community-serving elements such as affordable housing, health care facilities, educational institutions, and commercial spaces that create jobs. The flexible nature of QLICIs allows for multi-faceted development that addresses various community needs.

Leveraging Additional Financing

A QLICI can act as a critical piece in the capital stack that attracts other sources of funding. For example, the presence of a QLICI can help reassure other investors and lenders about the viability of a project, leading to increased overall investment.

Community Impact and Compliance Benefits

Projects funded through QLICIs are required to provide measurable community impacts. This aligns with the growing emphasis among developers and investors on social responsibility and impact investing. Additionally, engaging in projects that benefit communities living with low incomes can facilitate compliance with various regulatory requirements or corporate social responsibility goals.

For example, Capital Impact Partners closed on QLICI loans totaling $10.6 million to assist the Center for Transforming Lives in Fort Worth, Texas. The funding supported the conversion of a 102,000-square-foot warehouse into an early childhood education and economic mobility center, increasing childcare availability by 57 percent and boosting economic mobility services to 1,200 women by 65 percent annually. This initiative, crucially supported by NMTC, enabled the construction of a facility dedicated to breaking intergenerational poverty through programming that addresses physical, financial, and emotional needs.

QLICIs are a powerful tool in community development, providing critical financial incentives and benefits that support significant and impactful development projects in disinvested areas. For developers, the strategic use of QLICIs not only enhances the feasibility and scope of their projects but also contributes to their broader economic and social objectives, making them valuable partners in community revitalization efforts.

Check out our mission-driven lending page for more information about our products and to find out which might work best for you.

In this series about community development lending, we aim to shed light on the diverse types of loans we offer, in the hope that it will provide the clarity our borrowers need to make an informed decision about applying for a community development loan.

In this fifth installment, we explore an essential financial tool in community development: loan refinancing.

What is Loan Refinancing?

Loan refinancing in the context of community development involves replacing an existing debt obligation with another under different terms. This strategy is often used to secure lower interest rates, extend repayment terms, or access additional funds for project development. Refinancing can alleviate financial pressure, provide more favorable terms, and free up capital for further investment into community-centric projects. If approved, the borrower gets a new contract that takes the place of the original agreement.

Transforming Communities Through Strategic Refinancing

Refinancing can play a pivotal role in sustaining and scaling community development efforts. It offers developers the flexibility to adjust their financial strategies in response to changing market conditions or project needs, ensuring long-term project viability and impact.

The Benefits of Refinancing

Refinancing offers several advantages:

Reduced Costs: Lower interest rates can significantly decrease the overall cost of borrowing.

Improved Cash Flow: Extended loan terms provide developers with better cash flow management, enabling them to allocate resources more effectively across projects.

Strategic Allocation: Access to additional funds allows for investment in other critical aspects of development, such as predevelopment costs and new projects.

Example: Capital Impact Partners provided a $10 million loan to refinance an existing loan on a 45,252-square-foot property located in Los Angeles. This refinancing was strategically executed to replace the existing loan and secure additional capital for soft costs, predevelopment, and approvals necessary for transforming the property. This loan enabled the conversion of the current vacant buildings into a six-story, 252-unit multifamily, 100 percent affordable apartment building targeting tenants living with low and moderate incomes, addressing the acute demand for affordable housing in Los Angeles.

For community developers looking to maximize the impact of their projects, understanding and utilizing refinancing can be a game changer. By adjusting financial strategies to better suit their needs, developers can ensure the sustainability and expansion of their community initiatives.

Check out our mission-driven lending page for more information about our products and to find out which might work best for you.

Whether you’re a seasoned real estate developer fine-tuning your strategies or an aspiring newcomer eager to make your mark in the industry, there is always more to know and learn to help grow your business and scale your impact. This series is designed to provide invaluable insights and actionable advice to propel your development projects and your business forward.

At Capital Impact Partners, in particular, we offer flexible and affordable financing to a diverse array of community development projects that deliver tangible social impact. From community health centers to affordable housing developments, we are committed to empowering projects that uplift communities and foster sustainable growth. We also offer programmatic services that equip you with the resources, support, and networking opportunities you need to succeed in the real estate development world.

In the competitive realm of real estate development, success hinges not only on vision and execution but also on the ability to navigate complex relationships, craft solid projections, and attract investors. These pillars serve as the bedrock upon which thriving projects are built, distinguishing between mere ventures and enduring successes.

In this final installment of our series, let’s explore the key elements that set a developer up for attracting investors for real estate development, as well as strategies for anticipating and meeting their needs.

Financial Statements and Bankability

Ensuring that developers’ balance sheets and other financial statements accurately reflect their business’ health is paramount to attracting investors for real estate development. Lenders and investors look for reliability, organization, and trustworthiness when evaluating potential projects. By conveying a deep understanding of the project, its financing strategy, and the market, developers can instill confidence and mitigate lender scrutiny.

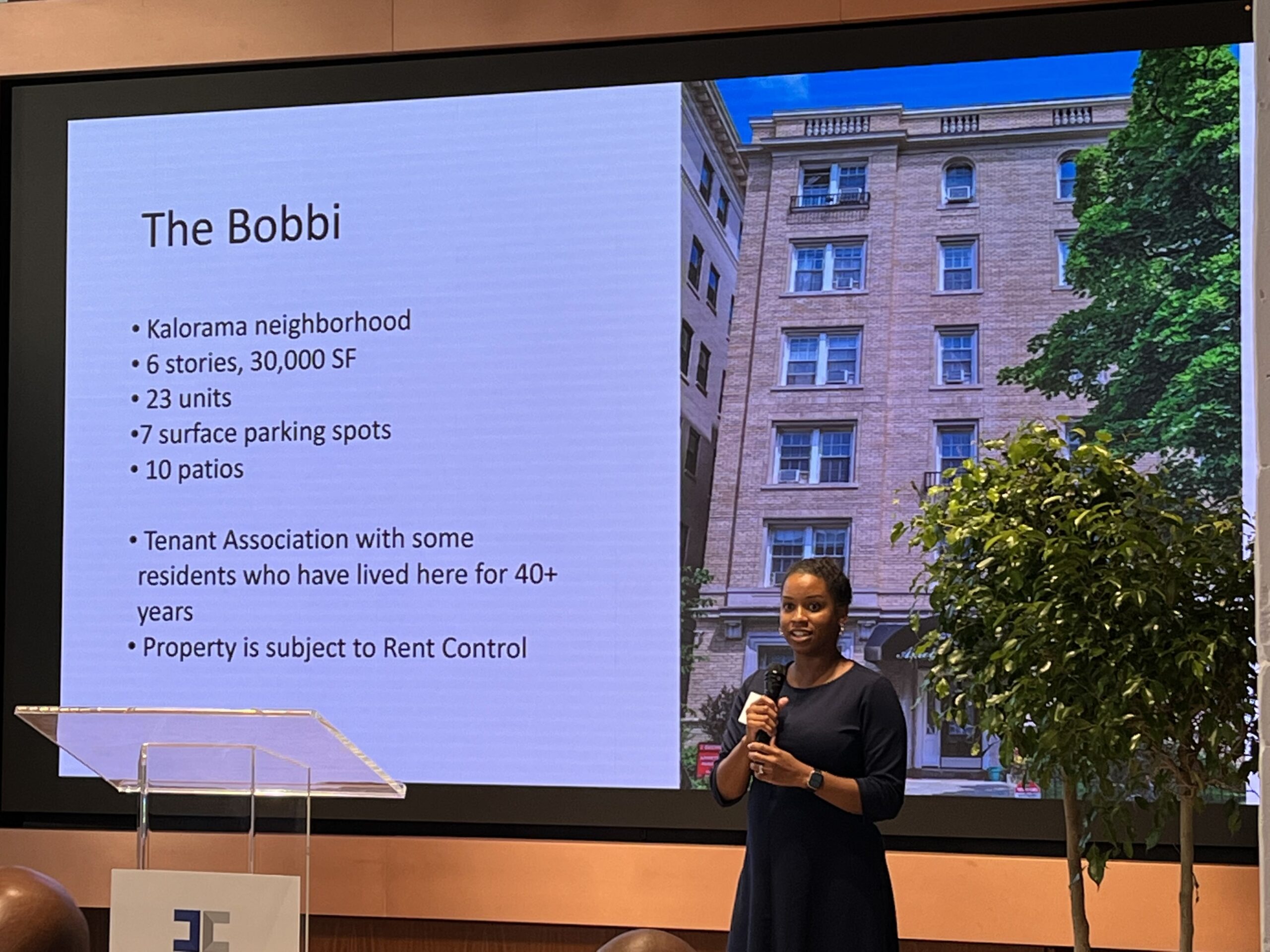

“For the Bobbi project, I was able to prepare for lender scrutiny by knowing the deal inside and out better than any consultants on my project, and being able to articulate the vision, the financing strategy, and the market.” – Ronette (Ronnie) C. Slamin, Founder and Principal at Embolden Real Estate

Slamin: Ensuring that developers’ balance sheets and other financial statements accurately reflect their business’ health is paramount to attracting investors for real estate development.

Anticipating Investor and Lender Needs

Before approaching lenders or investors, developers must ask themselves critical questions about their project and financing strategy. Being upfront about personal finances, including credit score and debt payment history, is essential for building trust and credibility. By aligning project goals with lender portfolios and understanding their business models, developers can tailor their pitches to meet lender and investor needs effectively.

Professional Patience and Effective Communication

Patience is a virtue in real estate development, particularly during the funding and underwriting phases. Rushing the underwriting process can lead to misunderstandings and delays, so developers must approach it with professionalism and collaboration. Maintaining effective communication, especially in challenging situations, is crucial for building strong relationships, attracting investors, and hence securing financing.

By emphasizing transparency, aligning with lender objectives, and fostering collaboration throughout the underwriting process, developers can forge robust partnerships with lenders and investors, ensuring the financing needed for their projects.

In this series about community development lending, we aim to shed light on the diverse types of loans we offer, in the hope that it will provide the clarity our borrowers need to make an informed decision about applying for a community development loan.

In this fourth installment, we take a look at business acquisition loans, a vital tool in the realm of community development allowing developers to broaden their reach and create lasting impact.

What is a Business Acquisition Loan?

A business acquisition loan is a financial instrument designed to provide funding for individuals or businesses to purchase an existing business. These loans are often sought by entrepreneurs looking to expand their business portfolio, individuals seeking to become business owners, or existing business owners interested in diversifying their operations by acquiring complementary businesses. In the case of community developers, the specific goal would be to further community development initiatives.

Two noteworthy business acquisition loans within the realm of community development, and which we offer at Capital Impact Partners, are cooperative loans, and working capital line of credit loans. One of the most significant steps a business can take is acquiring another business or securing essential working capital. These pivotal moments can be catalysts for growth, job creation, and lasting community impact.

Unlocking Opportunities Through Cooperative Business Acquisitions: Cooperative Business Loans

Cooperatives have long been champions of community-driven economic development. Whether it is workers seeking to purchase a business from their employer, or a group of farmers joining forces to better serve their local markets, business acquisitions can be a game-changer.

Broaden impact: acquiring an established business can expedite a cooperative’s growth and its ability to serve the community.

Leverage expertise: gain access to experienced staff, established customer bases, and valuable industry knowledge.

Ensure stability: preserve jobs, retain local ownership, and maintain the legacy of the business being acquired.

Capital Impact Partners has closed a business acquisition loan to Ward Lumber Worker Cooperative, Inc. (WLWC) to support the acquisition of 100 percent of the capital stock of Ward Lumber Co. (Ward), representing the conversion to employee ownership of the company and all of its assets. The transaction marked the first employee ownership transition, or worker co-op conversion, and the largest of its kind in the North Country region of New York State.

This business acquisition that led to Ward’s conversion to the employee ownership model helps to continue to support the region’s farm and construction industries, provide for above-average employee retention and wages, sustain the future of the enterprise, and build wealth in the community through ownership.

The Lifeline for Day-to-Day Operations: Working Capital Line of Credit Loans

In the ever-evolving world of business, maintaining a healthy cash flow is paramount. Working capital lines of credit are the financial lifelines that enable businesses to navigate the ebb and flow of daily operations effectively. These small-business loans are a type of short-term financing that is used to cover a business’s operating expenses, such as rent, payroll or inventory.

Working Capital Line of Credit loans offer several advantages:

Flexibility: borrow what you need when you need it, providing the agility required to seize opportunities or address unforeseen challenges.

Stabilizing cash flow: ensure that your business can cover operational expenses, pay suppliers, and meet payroll without interruptions.

Fueling growth: invest in inventory, equipment, or marketing initiatives that drive business expansion and community impact.

In 2020, Capital Impact Partners closed on a Working Capital Line of Credit loan to The Achievable Foundation (Achievable), an organization focused on health and wellness, and supportive services for people with disabilities based out of Los Angeles, California. A year prior, a few setbacks had negatively impacted the business including the loss of providers, amongst other difficulties. This line of credit allowed Achievable to replenish their cash and weather the operational challenges that emerged that year.

Working Capital Line of Credit loans represent a necessary lifeline for organizations such as Achievable, that more often than not find it challenging to receive financing from traditional lending institutions, particularly in rough times. This loan has helped Achievable stay operational, and carry out their mission of serving their communities.

Check out our mission-driven lending page for more information about our products to find out which might work best for you.

Whether you’re a seasoned real estate developer fine-tuning your strategies or an aspiring newcomer eager to make your mark in the industry, there is always more to know and learn to help grow your business and scale your impact. This series is designed to provide invaluable insights and actionable advice to propel your development projects and your business forward.

At Capital Impact Partners, in particular, we offer flexible and affordable financing to a diverse array of community development projects that deliver tangible social impact. From community health centers to affordable housing developments, we are committed to empowering projects that uplift communities and foster sustainable growth. We also offer programmatic services that equip you with the resources, support, and networking opportunities you need to succeed in the real estate development world.

In the competitive realm of real estate development, success hinges not only on vision and execution but also on the ability to navigate complex relationships, craft solid real estate development projections, and attract investors. These pillars serve as the bedrock upon which thriving projects are built, distinguishing between mere ventures and enduring successes.

Solid real estate development projections are a key to success, providing a roadmap for project feasibility and financial viability. In this installment, we’ll explore the critical aspects of creating pro forma models and building capital stacks, essential for navigating the complexities of the development process.

Creating Pro Formas: A Vital Tool for Success

A pro forma model is a financial projection tool that forecasts the potential financial outcomes of a real estate development project. It serves as a crucial guide for developers, investors, and lenders, offering insights into project feasibility and potential returns on investment. To create a robust pro forma model, developers must consider a range of factors, including land acquisition costs, construction expenses, operating expenses, and projected rental income.

Key Considerations in Pro Forma Development

Developers must carefully balance short-term and long-term real estate development projections in their pro forma models, taking into account factors such as vacancy rates, management costs, taxes, and rent projections based on cost per square foot. Challenges may arise during the creation and updating of pro forma models, requiring developers to adapt and address uncertainties effectively. Pre-development phase costs, including environmental reports and market studies, are crucial considerations that must be prioritized in pro forma development.

“One of the critical elements that need to be in your pro forma are projections into the future, which are costs and rent, and more importantly, how long it’s going to take.” – Christopher Agorsor, Principal at Agorsor Equities

Agorsor: Solid real estate development projections are a key to success, providing a roadmap for project feasibility and financial viability.

Lessons Learned and Tips for Success

Throughout the development process, developers must remain vigilant and adaptable, learning from their experiences and refining their strategies for future projects. Transparency and open communication with lenders are essential for building strong relationships and securing project financing. By attending industry events, networking, and staying informed about market conditions, developers can streamline their capital stacks and secure financing tailored to their project’s needs.

Building Capital Stacks: Navigating Project Financing

A capital stack represents the various sources of funding, including debt and equity, that finance a real estate development project. Developers must carefully structure their capital stacks to ensure project feasibility and mitigate risk.

By mastering the art of pro forma development and capital stack structuring, developers can navigate the complexities of the development process with confidence and achieve their goals. Training and resources provided through our programmatic services will help give you the confidence needed to build solid projections.

Whether you’re a seasoned real estate developer fine-tuning your strategies or an aspiring newcomer eager to make your mark in the industry, there is always more to know and learn to help grow your business and scale your impact. This series is designed to provide invaluable insights and actionable advice to propel your development projects and your business forward.

At Capital Impact Partners, in particular, we offer flexible and affordable financing to a diverse array of community development projects that deliver tangible social impact. From community health centers to affordable housing developments, we are committed to empowering projects that uplift communities and foster sustainable growth. We also offer programmatic services that equip you with the resources, support, and networking opportunities you need to succeed in the real estate development world.

In the competitive realm of real estate development, success hinges not only on vision and execution but also on the ability to ensure real estate development relationship building, craft solid projections, and attract investors. These pillars serve as the bedrock upon which thriving projects are built, distinguishing between mere ventures and enduring successes.

Real estate development relationship building is the cornerstone of success in the field, spanning two critical areas: building a stellar development team, and engaging local stakeholders and the community. Let’s delve into each of these aspects to understand their significance and how they contribute to project success.

Building a Stellar Development Team

Real estate development relationship building starts with building a great team. A successful development project begins with assembling a stellar team that shares your vision and values. From project managers to architects, each team member plays a vital role in bringing your vision to life. As a new developer, being actively involved in the team-building process is essential. Seek out experienced professionals who align with the specific needs of your project, whether it’s historic preservation or meeting energy requirements. By asking for references and recommendations and ensuring each team member is comfortable and capable in their role, you can build a cohesive team poised for success.

Slamin: Engaging with local stakeholders and the community is fundamental to the success of real estate developers.

Engaging Local Stakeholders and Community

Engaging with local stakeholders and the community is not just a box to check—it’s a fundamental aspect of successful real estate development. From the early stages of planning to project completion, involving the community in the decision-making process is essential for building trust and goodwill. Define ‘community’ in the context of your project and understand the unique dynamics at play. Be deliberate in your outreach efforts, ensuring that community input informs every stage of the project lifecycle. While challenges may arise, proactive engagement and genuine listening can help overcome obstacles and foster meaningful connections.

As you embark on your journey as a real estate developer, remember that success is built on relationships. Whether it’s with your development team, lenders, or the local community, cultivating strong connections is essential to bringing your vision to life.

In this series about community development lending, we aim to shed light on the diverse types of loans we offer, in the hope that it will provide the clarity our borrowers need to make an informed decision about applying for a community development loan.

In this third installment, we turn our attention to construction loans, the financial cornerstone that transforms plans into reality and buildings into vibrant community assets.

What is a Construction Loan?

A construction loan is a short-term loan that propels your development project from the drawing board to a physical structure. It provides the necessary funding to cover the costs associated with building, renovating, or expanding community assets. Construction loans may also cover the costs of buying land, drafting plans, taking out permits and paying for labor and materials. Construction loans typically have higher interest rates than other types of loans because lenders are taking on more risk by financing the construction of a new property.

Turning Blueprints Into Bricks

At the heart of any community development project lies the construction phase. This is where ideas take shape, and communities begin to witness tangible progress. Construction loans provide the essential capital for hiring contractors, purchasing materials, and overseeing the entire construction process. They also empower developers to maintain high standards of quality by financing skilled labor, sustainable materials, and adherence to safety standards. Moreover, construction loans cover costs at various stages of construction, from groundbreaking to final touches, keeping the project on track and minimizing delays so communities can start benefiting sooner.

How are Construction Loans Used in Community Development?

Construction loans enable developers to borrow money to purchase materials and pay for labor necessary to build or rehabilitate a real estate project. Unlike traditional loans, construction loans are tailored to the unique financial needs and timelines of development projects, ensuring that funds are available precisely when they’re needed the most. Because construction loans generally are intended to cover the building process, they’re typically issued for a period of 12 to 18 months. Community developers can use construction loans towards projects such as building or rehabilitating spaces into affordable housing. Capital Impact Partners has closed on a loan to finance the construction of a 37-unit apartment building for veterans and their families living with very low incomes and experiencing homelessness. Once completed, the six-story, 28,0000-square-foot apartment building in the Brightwood Park neighborhood of D.C. will play an important role in building the resilience of the local community.

Construction loans can be used towards the rehabilitation or construction of charter schools as well. Capital Impact Partners has closed on a construction loan to fund the renovation of a 25,000-square-foot former Kaplan College into the Betty M. Condra School for Education (Condra School) in Lubbock, Texas. When complete, the renovations will allow the Condra School to increase its capacity by 88 percent to 375 students, with larger classrooms and more play spaces to benefit students with attention-deficit/hyperactivity disorder (ADHD).

Flexible, Short-term Financing for Long-term Impact

In the case of a construction loan, disbursement happens in phases. This means that the lender pays the developer in installments, called “draws,” instead of transferring a lump sum. This is to ensure that the developer is using the loan funds for the intended purpose. Each installment coincides with an important phase of the project, such as pouring the foundation, framing, and finishing work.

One benefit of construction loans is that developers would only pay interest on installments that have been drawn, versus paying interest on the entire loan amount. Another benefit is that construction loans offer more flexibility in terms of loan terms, compared to traditional loans. Developers can make loan terms around the needs of their projects.

Check out our mission-driven lending page for more information about our products to find out which might work best for you.

In this series about community development lending, we aim to shed light on the diverse types of loans we offer, in the hope that it will provide the clarity our borrowers need to make an informed decision about applying for a community development loan.

In this second installment, we explain what real estate acquisition loans are, and how developers and community leaders can utilize them to bring their community-centered projects to life.

What is a Real Estate Acquisition Loan?

A real estate acquisition loan is a type of loan that is used to purchase real estate. This type of loan is often used by community developers to acquire existing property or development land that they plan to preserve or redevelop for affordable housing, commercial development, or other community-benefit purposes.

How are Real Estate Acquisition Loans Used in Community Development?

Real estate acquisition loans can be used to purchase a variety of properties, including:

Vacant land for the development of new affordable housing, commercial space, or other community facilities

Existing buildings that will be renovated or converted into community facilities

Distressed properties that need to be rehabilitated or redeveloped to revitalize a neighborhood or community

Vacant land for the development of new affordable housing, commercial space, or other community facilities

Capital Impact Partners has closed on a real estate acquisition loan to Medici Road to purchase a vacant plot in Washington D.C.’s Ward 7. Medici Road plans to develop the land into a 17,000-square-feet building with 12 condo units for sale at prices affordable to D.C. residents earning 80 percent of the Area Median Income – a path to intergenerational wealth building, and a way for long-time residents to stay local in a gentrifying neighborhood.

Existing buildings that will be renovated or converted into community facilities

The Betty M. Condra School for Education Innovation in Lubbock, Texas, was acquired with a real estate acquisition loan issued by Capital Impact Partners. The acquisition of this two-story building increases the school’s capacity by 70 percent.

Distressed properties that need to be rehabilitated or redeveloped to revitalize a neighborhood or community

An illustrative example is that of Skyland Apartments in Washington, D.C. ‘s Ward 8, which was acquired by Enterprise Community Development (ECD), a leading nonprofit affordable housing development firm in the Mid-Atlantic region. With an acquisition loan issued by Capital Impact Partners, ECD’s development of Skyland Apartments preserves 224 affordable residential units and eight commercial units. The residential units are occupied by families earning at or below 60 percent of the local Area Median Income.

Access to Capital, Flexibility, and Partnership Building

Real estate acquisition loans can provide a number of benefits for community development projects. They can provide community developers with the financial resources they need to purchase land or properties that they might not be able to afford otherwise. The flexibility of being able to purchase any property allows community developers to tailor their projects to the specific needs of the communities they serve.

Real estate acquisition loans can also help community developers to build partnerships with other organizations, such as lenders, investors, and government agencies. These partnerships can provide additional resources and support for community development projects.

Check out our mission-driven lending page for more information about our products to find out which might work best for you.

Launching and growing a food business requires significant upfront investment – but obtaining the funds to get one off the ground is a challenge for many start-up founders. This is especially true for diverse entrepreneurs, who face systemic challenges in accessing business funding, including grants and loans.

That’s where the Nourish DC Collaborative comes in. Since 2021, it has deployed $935,000 in grant funding over two rounds to 22 diverse-owned businesses (15 of which are also woman-owned). In addition to these grants — which are rarely an option in the food industry — Nourish DC has offered $15 million in loan financing and $625,000 in funding to help partners increase their technical assistance and lending capacity.

Funding That Fuels Communities

Nourish DC grants are available to D.C. businesses ranging from grocery stores to urban farms, food processors, and restaurants that increase access to healthy food and create high-quality jobs in the community. All current grantees are located in Supermarket Tax Incentive Areas (neighborhoods with poor access to groceries and fresh food), primarily in the District’s Wards 5, 7, and 8.

The grants can be a lifeline for founders in the early stages of starting a business who may not qualify for loans.

“Many of our grantees are receiving their first grants, which gives them the confidence and validation to grow their businesses,” says Alison Powers, director of Economic Opportunities for Capital Impact Partners.

Since community members are better placed to understand their neighbors’ needs than funders, Nourish DC grants are responsive and inclusive, allowing recipients to direct the funds in the ways that will most benefit their businesses and communities.

Grantee Story: Turning a Family Food Tradition Into a Business

When D.C. native Patrice Cunningham lost her job as chef and manager of a Korean BBQ restaurant in the District at the start of the COVID-19 pandemic, she saw a moment of opportunity.

Cunningham held an MBA and had long dreamed of starting a business that celebrated the foods from her blended Korean and African-American heritage. In the summer of 2020, she landed on a plan: selling fresh kimchi using her mother’s recipe. With the U.S. market for kimchi — a traditional Korean dish made of salted and fermented cabbage and other vegetables — valued at $70 million, Cunningham knew that her idea had potential. But securing funding for her new business, which she named Tae-Gu Kimchi for her mother’s hometown in South Korea, wasn’t so easy.

Facing Financial Headwinds

From the start, Cunningham hoped to create a national brand and see Tae-Gu Kimchi on grocery shelves across the country in stores like Whole Foods and Trader Joe’s. But when she lost her job, Cunningham only had $500 in her bank account. To cover start-up costs, including licensing fees, supplies, packaging, and commercial kitchen space, she accepted a loan from a friend and maxed out her credit cards. Her mother pitched in to buy ingredients and help her make the kimchi.

Cunningham’s initial weekly sales at farmers markets were enough to cover ingredients for the next week’s batch of kimchi — but her reliance on revenue meant she couldn’t scale up or work toward her goal of getting her product onto store shelves.

The obstacles Cunningham faced weren’t unique. In addition to difficulty accessing credit, diverse-owned businesses nationwide hold fewer cash reserves and report lower first-year profits, factors which can curtail a business’ ability to grow and even to survive long-term.

But when Cunningham was awarded a $45,000 Nourish DC grant in early 2023, Tae-Gu Kimchi’s trajectory changed quickly.

“It was like winning the golden ticket,” Cunningham said. “It was pivotal because I was ‘bootstrapping’ at that point. I had all these costs, and I had run out of packaging.”

Preparing For Scale

With Nourish DC grant funding in hand, Cunningham went from selling kimchi at four farmer’s markets per week to 15. She purchased a truck, additional tents and tables, more packaging (featuring a brand redesign), and commercial refrigeration space. She also immersed herself in courses and programs about everything from packaging to pitching her product to grocery stores.

Since Cunningham’s mother had always made kimchi from memory, one key challenge was scaling her recipe. Cunningham carefully documented her process and the exact mix of ingredients that made the kimchi stand out. “That taste is something you can never forget,” she says.

Tae-Gu Kimchi’s growth has allowed Cunningham to build a sales team of nine employees and a kitchen team of three in addition to herself, expanding the Nourish DC grant’s impact.

Growing Within the D.C. Community

When small businesses succeed, they create a rising tide that lifts those around them. Nourish DC grant recipients don’t just provide their communities with additional food options, but also with job opportunities and chances for neighbors to get to know one another.

In the last year, Tae-Gu Kimchi’s growth has allowed Cunningham to build a sales team of nine employees and a kitchen team of three in addition to herself, expanding the Nourish DC grant’s impact. She also used to grant funding to dramatically scale up her farmers’ market business, going from four markets per week to 15 and hiring a company to set up and manage these. This gave her more time to pursue grocery sales channels, manage online sales, and develop content for social media.

With Nourish DC grant funding in hand, Cunningham went from selling kimchi at four farmers’ markets per week to 15.

Cunningham has deep appreciation for Nourish DC and the support she received. “They understand that DC is a big food scene right now and so many people are starting food businesses,” she says. “They give businesses the opportunity to make it.”

The Nourish DC grant had the desired impact. As of 2023, Cunningham’s various sales channels — farmers’ markets, grocery stores (her products are sold at two Dawson’s Markets in the DC area), and online sales — are consistently producing revenue of $15,000 to $20,000 per month, with a few months spiking upwards of $30,000. Local customers also can pick up the kimchi at her Ward 5 location or have it delivered.

Now, Cunningham is looking for the capital to fuel her next round of growth, which will include building her own kimchi kitchen/production facility, identifying a co-packing partner, and making inroads into retail channels. “I’m going to take this as far as I can,” she says.

In this series about community development lending, we aim to shed light on the diverse types of loans we offer at Capital Impact Partners, in the hope that it will provide the clarity our borrowers need to make an informed decision about applying for a community development loan. In this first installment, we delve into the essence of predevelopment loans, exploring what they are and how developers and community leaders can utilize them to bring their community-centered projects to life.

What is a Predevelopment Loan?

A predevelopment loan serves as a critical lifeline during the earliest stages of a development project. It specifically targets the upfront costs associated with project planning and preparation, enabling developers to refine their visions and align them with the needs and aspirations of the communities they aim to serve. This loan bridges the gap between concept and execution, ensuring a solid foundation for success.

Exploring Site Selection and Due Diligence

Choosing the right location is paramount in community development projects. Predevelopment loans allow developers to explore potential sites, conduct due diligence, and assess the feasibility of their projects; this phase involves considerable research and assessment. From evaluating zoning regulations and environmental factors to assessing community demographics and market demand, developers can make informed decisions that contribute to the long-term success of their initiatives.

Capital Impact has financed a predevelopment loan to Chestnut Neighborhood Revitalization Corporation (CNRC) to assess the feasibility of constructing The Ivory, a five-story, mixed-used, mixed-income development in the Chestnut neighborhood of Austin, Texas. The Ivory’s construction is expected to preserve the history, legacy, and culture of Chestnut, once a flourishing artistic, cultural, and commercial hub for the African-American community.

Engaging Stakeholders and Building Partnerships

Predevelopment loans not only provide the financial means for planning but also facilitate collaboration and partnership building. Developers can leverage these loans to engage with stakeholders, including community members, local organizations, and government agencies. Through consultations, workshops, and community meetings, developers can gather valuable input, build consensus, and establish partnerships that enhance the overall project design and increase its positive impact.

An illustrative example is Russell Woods, a 102-unit assisted living senior housing development located in Detroit. Capital Impact has financed a predevelopment loan to Icon Heritage Partners to ensure that collaboration with the City of Detroit was established so that the renovation of the property fit within the city’s Strategic Neighborhood Plan.

Navigating Regulatory Requirements and Permitting

Complying with regulatory requirements and obtaining necessary permits can be complex and time-consuming. Predevelopment loans enable developers to navigate these processes efficiently by allocating funds for legal and consulting services, permit fees, and other regulatory expenses. This support streamlines the development timeline and minimizes potential obstacles, ensuring smoother project progression.

Mitigating Risks and Demonstrating Viability

Developing a successful community-centered project involves potential risks. Predevelopment loans mitigate these risks by providing financial resources to overcome obstacles encountered during the planning phase. By demonstrating project viability and commitment, developers enhance their credibility when seeking additional financing from lenders or investors for subsequent project stages.

TBV Courtyard, a 12-unit affordable multifamily development in the South Annex neighborhood of Richmond, California, is a great example of how additional project financing comes more easily when project viability is demonstrated. TBV Courtyard represents phase two of a larger development plan to provide a total of 105 units of affordable housing to the neighborhood. Given that phase one’s predevelopment studies proved viable, the process to receive financing for phase two was seamless.

Check out our mission-driven lending page for more information about our products to find out which might work best for you.

Stay tuned for the next installment in our blog series, where we explore real estate acquisition loans, another type of loan that moves community development projects forward.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.