In this series about community development lending, we aim to shed light on the diverse types of loans we offer, in the hope that it will provide the clarity our borrowers need to make an informed decision about applying for a community development loan.

In this second installment, we explain what real estate acquisition loans are, and how developers and community leaders can utilize them to bring their community-centered projects to life.

What is a Real Estate Acquisition Loan?

A real estate acquisition loan is a type of loan that is used to purchase real estate. This type of loan is often used by community developers to acquire existing property or development land that they plan to preserve or redevelop for affordable housing, commercial development, or other community-benefit purposes.

How are Real Estate Acquisition Loans Used in Community Development?

Real estate acquisition loans can be used to purchase a variety of properties, including:

Vacant land for the development of new affordable housing, commercial space, or other community facilities

Existing buildings that will be renovated or converted into community facilities

Distressed properties that need to be rehabilitated or redeveloped to revitalize a neighborhood or community

Vacant land for the development of new affordable housing, commercial space, or other community facilities

Capital Impact Partners has closed on a real estate acquisition loan to Medici Road to purchase a vacant plot in Washington D.C.’s Ward 7. Medici Road plans to develop the land into a 17,000-square-feet building with 12 condo units for sale at prices affordable to D.C. residents earning 80 percent of the Area Median Income – a path to intergenerational wealth building, and a way for long-time residents to stay local in a gentrifying neighborhood.

Existing buildings that will be renovated or converted into community facilities

The Betty M. Condra School for Education Innovation in Lubbock, Texas, was acquired with a real estate acquisition loan issued by Capital Impact Partners. The acquisition of this two-story building increases the school’s capacity by 70 percent.

Distressed properties that need to be rehabilitated or redeveloped to revitalize a neighborhood or community

An illustrative example is that of Skyland Apartments in Washington, D.C. ‘s Ward 8, which was acquired by Enterprise Community Development (ECD), a leading nonprofit affordable housing development firm in the Mid-Atlantic region. With an acquisition loan issued by Capital Impact Partners, ECD’s development of Skyland Apartments preserves 224 affordable residential units and eight commercial units. The residential units are occupied by families earning at or below 60 percent of the local Area Median Income.

Access to Capital, Flexibility, and Partnership Building

Real estate acquisition loans can provide a number of benefits for community development projects. They can provide community developers with the financial resources they need to purchase land or properties that they might not be able to afford otherwise. The flexibility of being able to purchase any property allows community developers to tailor their projects to the specific needs of the communities they serve.

Real estate acquisition loans can also help community developers to build partnerships with other organizations, such as lenders, investors, and government agencies. These partnerships can provide additional resources and support for community development projects.

Check out our mission-driven lending page for more information about our products to find out which might work best for you.

In this series about community development lending, we aim to shed light on the diverse types of loans we offer at Capital Impact Partners, in the hope that it will provide the clarity our borrowers need to make an informed decision about applying for a community development loan. In this first installment, we delve into the essence of predevelopment loans, exploring what they are and how developers and community leaders can utilize them to bring their community-centered projects to life.

What is a Predevelopment Loan?

A predevelopment loan serves as a critical lifeline during the earliest stages of a development project. It specifically targets the upfront costs associated with project planning and preparation, enabling developers to refine their visions and align them with the needs and aspirations of the communities they aim to serve. This loan bridges the gap between concept and execution, ensuring a solid foundation for success.

Exploring Site Selection and Due Diligence

Choosing the right location is paramount in community development projects. Predevelopment loans allow developers to explore potential sites, conduct due diligence, and assess the feasibility of their projects; this phase involves considerable research and assessment. From evaluating zoning regulations and environmental factors to assessing community demographics and market demand, developers can make informed decisions that contribute to the long-term success of their initiatives.

Capital Impact has financed a predevelopment loan to Chestnut Neighborhood Revitalization Corporation (CNRC) to assess the feasibility of constructing The Ivory, a five-story, mixed-used, mixed-income development in the Chestnut neighborhood of Austin, Texas. The Ivory’s construction is expected to preserve the history, legacy, and culture of Chestnut, once a flourishing artistic, cultural, and commercial hub for the African-American community.

Engaging Stakeholders and Building Partnerships

Predevelopment loans not only provide the financial means for planning but also facilitate collaboration and partnership building. Developers can leverage these loans to engage with stakeholders, including community members, local organizations, and government agencies. Through consultations, workshops, and community meetings, developers can gather valuable input, build consensus, and establish partnerships that enhance the overall project design and increase its positive impact.

An illustrative example is Russell Woods, a 102-unit assisted living senior housing development located in Detroit. Capital Impact has financed a predevelopment loan to Icon Heritage Partners to ensure that collaboration with the City of Detroit was established so that the renovation of the property fit within the city’s Strategic Neighborhood Plan.

Navigating Regulatory Requirements and Permitting

Complying with regulatory requirements and obtaining necessary permits can be complex and time-consuming. Predevelopment loans enable developers to navigate these processes efficiently by allocating funds for legal and consulting services, permit fees, and other regulatory expenses. This support streamlines the development timeline and minimizes potential obstacles, ensuring smoother project progression.

Mitigating Risks and Demonstrating Viability

Developing a successful community-centered project involves potential risks. Predevelopment loans mitigate these risks by providing financial resources to overcome obstacles encountered during the planning phase. By demonstrating project viability and commitment, developers enhance their credibility when seeking additional financing from lenders or investors for subsequent project stages.

TBV Courtyard, a 12-unit affordable multifamily development in the South Annex neighborhood of Richmond, California, is a great example of how additional project financing comes more easily when project viability is demonstrated. TBV Courtyard represents phase two of a larger development plan to provide a total of 105 units of affordable housing to the neighborhood. Given that phase one’s predevelopment studies proved viable, the process to receive financing for phase two was seamless.

Check out our mission-driven lending page for more information about our products to find out which might work best for you.

Stay tuned for the next installment in our blog series, where we explore real estate acquisition loans, another type of loan that moves community development projects forward.

For anyone seeking to access lending for community development projects, understanding the different types of loans can be confusing.

At Capital Impact Partners, our commitment to fostering positive social impact drives us to support mission-aligned real estate developers and community development leaders with a range of flexible and affordable financing solutions.

Our community development lending offerings include predevelopment loans, real estate acquisition loans, construction loans, working capital loans, refinance loans, New Market Tax Credit (NMTC) leverage loans, and NMTC Qualified Low-Income Community Investment (QLICI) loans.

Our loan products are designed to help our borrowers achieve their goals and revitalize disinvested and underestimated communities, whether that constitutes developing or preserving affordable housing, creating jobs through a small business, or building the resilience of communities through access to health care, healthy food, and education.

In this series of blogs, we aim to shed light on the diverse types of loans we offer and explore their significance within the context of Capital Impact’s mission-driven financing, in the hope that it will provide clarity to help borrowers make informed decisions about applying for community development loans.

We walk through the different types of loans we use to support developers and community leaders in bringing their community-centered projects to life:

As a mission-driven developer, organization, or business looking into community development projects, you may be coming across language that might sound confusing and be challenging to understand. What is a CDFI? What is NMTC? What is LTV?

At Capital Impact Partners specifically, we offer flexible and affordable financing to a broad range of community development projects that deliver social impact, including community health centers, public charter schools, small businesses, cooperatives, healthy food retailers, affordable housing developments, and dignified aging facilities.

This glossary aims to demystify terms to help you navigate through our lending and programmatic services and offerings. Below you will find definitions of terms divided into the following thematic sections:

Community Development Financial Institutions (CDFIs)

Community Development Financial Institutions (CDFIs) are mission-driven private sector financial institutions that focus on serving people living with low incomes and people who have historically been locked out of the financial system. Their work entails providing lending for small businesses and community projects, affordable housing, and essential community services in the United States.

As a CDFI, Capital Impact Partners has delivered community facility financing, capacity-building programs, and impact investing opportunities to champion key issues of equity and social and economic justice since 1982.

Community Development

Community development activities tackle underestimated populations that do not have equitable access to affordable housing, health care, healthy food, and education, nor connections to capital, entrepreneurship, and quality jobs, to help them become stronger and more resilient.

At Capital Impact Partners, and together with the Momentus Capital branded family of organizations, we offer a continuum of capital products and services to transform how capital and investments flow into underestimated communities and drive community-led solutions that support economic mobility and wealth creation.

Lending Process

Capital Stack

Debt coverage ratio (DCR) is a measurement of a firm’s available cash flow to pay current debt obligations. While a DCR of 1.25 is the minimum requirement for most lenders, a higher number — such as 2 — shows lenders you are financially stable and can repay your debts. A higher DCR can also mean a potentially lower interest rate as lenders see you as less of a risk for defaulting on your loan.

Loan Term

The term of a loan is the period of time a borrower has to repay the loan. This choice affects their monthly principal and interest payment, their interest rate, and how much interest they will pay over the life of the loan.

A term sheet is a nonbinding agreement that shows the basic terms and conditions of an investment. The term sheet serves as a template and basis for more detailed, legally binding documents. Once the parties involved reach an agreement on the details laid out in the term sheet, a binding agreement or contract that conforms to the term sheet details is drawn up.

Underwriting

Underwriting is the process of your lender verifying your income, assets, debt, credit, and property details to issue final approval on your loan application.

Loan Types

Predevelopment Loan

A predevelopment loan serves as a critical lifeline during the earliest stages of a development project. It specifically targets the upfront costs associated with project planning and preparation, enabling developers to refine their visions and align them with the needs and aspirations of the communities they aim to serve. This loan bridges the gap between concept and execution, ensuring a solid foundation for success.

Real Estate Acquisition Loan

A real estate acquisition loan is a type of loan that is used to purchase real estate. This type of loan is often used by community developers to acquire existing property or development land that they plan to preserve or redevelop for affordable housing, commercial development, or other community-benefit purposes.

Construction Loan

A construction loan is a short-term loan that propels your development project from the drawing board to a physical structure. It provides the necessary funding to cover the costs associated with building, renovating, or expanding community assets. Construction loans may also cover the costs of buying land, drafting plans, taking out permits and paying for labor and materials. Construction loans typically have higher interest rates than other types of loans because lenders are taking on more risk by financing the construction of a new property.

Business Acquisition Loan

A business acquisition loan is a financial instrument designed to provide funding for individuals or businesses to purchase an existing business. These loans are often sought by entrepreneurs looking to expand their business portfolio, individuals seeking to become business owners, or existing business owners interested in diversifying their operations by acquiring complementary businesses. In the case of community developers, the specific goal would be to further community development initiatives.

Loan Refinancing

A refinance refers to the process of revising and replacing the terms of an existing credit agreement. Borrowers usually choose to refinance a loan seeking to make favorable changes to their interest rate, payment schedules, or other terms outlined in their contract. If approved, the borrower gets a new contract that takes the place of the original agreement.

New Market Tax Credit (NMTC) Qualified Low-Income Community Investment (QLICI) Loan

The capital that a community development entity provides to a qualifying project is known as a Qualified Low-Income Community Investment (QLICI) and it is a seven-year, interest-only loan.

Health Care

Integrated Care

Integrated care is a unique approach to health care that is characterized by close collaboration and communication between multiple doctors and healthcare professionals. In other words, it is a type of healthcare where all of your doctors work together to solve issues with your physical, mental, and behavioral health. At Capital Impact, we support the Integrated Care model because it improves the quality of care, promotes better health and lower costs while creating thousands of jobs, spurring economic development.

PACE (Program of All-inclusive Care for the Elderly)

Area Median Income is the income for the median household in a given region. If you were to line up each household from poorest to wealthiest, the household in the very middle would be considered the median.

Tenant Opportunity to Purchase Act (TOPA)

TOPA, or “Tenant Opportunity to Purchase Act”, is a type of anti-displacement housing policy that gives tenants options to have secure housing when the property they rent goes up for sale, while also preserving affordable housing.

Cooperatives

Food Co-ops

A food co-op is a grocery store that is totally independent and owned by the community members who shop there. An illustrative example is ChiFresh Kitchen, a food co-op owned by justice-involved Chicagoans. ChiFresh won a Co-op Innovation Award and was not only able to continue its expansion, but also pivot to provide freshly cooked and culturally appropriate foods to those impacted by COVID-19.

Housing Co-ops

A housing co-op provides an alternative to the traditional methods of acquiring a primary residence. It is a type of residential housing option that is actually a corporation whereby the owners do not own their units outright. Instead, each resident is a shareholder in the corporation based in part on the relative size of the unit that they live in. Capital Impact Partners has helped ROC USA, a nonprofit that helps residents form cooperative corporations to purchase their manufactured home communities from private owners and manage their neighborhoods in perpetuity. They have gone on to become a powerhouse in this area, helping thousands of residents become homeowners and community stewards.

Worker Co-ops

Worker cooperatives are values-driven businesses that are owned and operated by their employees. Capital Impact has made a $1 million preferred equity investment in Obran Cooperative, a unique company that operates a number of worker-owned healthcare companies.

Worker Co-op Conversions

Worker co-op conversions – or employee ownership conversions – occur when businesses transition from a traditional ownership structure to employee ownership. Essentially, the business owner sells the business to the employees. These conversions (PDF) can drive company productivity while rewarding the people who are contributing to the company’s success, as well as helping to preserve the company’s mission and values.

In 2021, Capital Impact Partners financed the worker co-op conversion of Ward Lumber. This new cooperative is another example of the power of worker co-op conversion to maintain and increase wealth and stability within communities.

Across the Momentus Capital branded family of organizations, we know that to maximize our impact, we need to first understand it. Building and sustaining healthy, inclusive, and equitable communities requires capital and resources – but without measuring outcomes, it’s impossible to develop effective interventions at scale.

That’s why we’ve developed a comprehensive Impact Framework to help us track the results of not only our loan offerings but also the capacity-building programs, technical assistance, and tools that make up our continuum of capital (PDF).

This framework is at the center of our decision-making process as we work toward our mission of helping to build inclusive and equitable communities by providing people access to the capital and opportunities they deserve.

So, what are we measuring, and why?

To learn more about what we are measuring and why, read the full article on Momentus Capital’s blog.

Across the Momentus Capital branded family of organizations, our mission is to ensure people and communities have the capital and opportunities they deserve to overcome a history of systemic disinvestment.

To support underestimated communities in achieving positive social and economic outcomes, we need a shared understanding of what that looks like, and why those outcomes are so important. This blog will outline how we at Momentus Capital define economic stability and why it is important, how it is tied to the other social determinants of health, and how we are working to promote economic stability through our work.

By Alexander McDonald, Senior Director of Lending Operations

For communities to thrive, they need resources — but too often, small business owners, developers, and local community development leaders lack access to the capital they need to drive progress.

Across the Momentus Capital branded family of organizations we are on a mission to change that through a community-first approach to lending grounded in our commitment to diversity, equity, and inclusion. And for us, that includes much more than the actual continuum of capital we deliver, but also HOW engage with our borrowers and partners to do that. Every aspect of our lending operations is built on our values, which means taking out a loan from Momentus is a much different experience than borrowing from a traditional financial institution.

But our approach doesn’t just feel good. It also leads to exceptional outcomes. The secret to our success? Putting the borrower first with superior client service, competitive products, and scaffolded support.

And our lending operations team is at the heart of what makes Momentus unique.

To learn more about how our lending operations team works with borrowers and supports social impact, please read our full blog on the Momentus Capital website.

Since our inception, we have served sectors, industries, and borrowers not served by the traditional financial system.

Like many CDFIs, Capital Impact provides more flexibility than traditional lenders in some key areas like loan-to-value limits and financial covenants that borrowers must meet.

However, our credit guidelines – the policies that guide our loan structures and lending decisions – are built on the traditional approach to credit that has deep roots in a financial system that intentionally excluded some people for much of its history. Often, our lending team seeks one or several “exceptions” to our credit guidelines to accommodate the diverse needs of our borrowers.

Creating flexible financing is both a mindset and an approach. To do so, we need input from our clients and communities to rethink and reshape our products and requirements. When done correctly, this approach gears us away from the extractive patterns of traditional financing and closer to confirming that when people are given the opportunity to succeed, their communities, local residents, and our country thrive.

We have spent the last several years providing capacity building and support to community-rooted developers across the country. Having seen in our own lending that these developers were not well represented and hearing the barriers that they face in scaling up to work on more and larger projects, we determined that we needed to take bigger steps to address the need.

How We Are Doing Things Differently

In that light, we spent the better part of 2022 reviewing and revising our lending requirements and processes to be more equitable, to better support community-rooted developers and borrowers from all walks of life in having access to the capital and opportunities they deserve.

As a part of the Momentus Capital branded family of companies, it also became important for Capital Impact to revise and improve efficiencies in lending approval processes to account for a combined strategy.

Because one of the most important parts of transformation is transparency, we want to share the recent updates to our credit guidelines with our communities, partners, and other stakeholders.

EDI program graduates benefit from training and access to capital.

An Overview of Our New Credit Guidelines

Equity Commitment

Developer Experience

Staying true to our vision, we want to be able to support community-centric developers who might not have had the opportunity to build and sustain a track record in the markets where they are active.

Old guideline: requirement of three completed and operating projects

New guideline: one completed project and have been in operation for 3+ years

We are committed to looking at the borrower as a whole, taking into account their background including education, work history, participation in the EDI program or other capacity building initiatives, as well as any relevant experience with joint venture partners and consultants.

Developer Equity

We wanted to lighten the load on a borrower to bring a certain amount of cash to each project.

Old guideline: 25 percent equity requirement for predevelopment costs in cases where there is real estate collateral

New guideline: 10 percent equity requirement for predevelopment costs

This change benefits borrowers by allowing them to preserve their funds and use them toward working capital, growing/expanding their business, hiring staff, etc.

Guarantee Requirements

Given that most of the borrowers we work with have limited resources, we have eliminated the requirement of a strong guarantor possessing liquid assets and cash flows.

We still expect people who own 20+ percent of a business and are actively engaged in the business to issue guarantees, but we now look at guarantees as an assurance of the borrower’s commitment to the project rather than as a source of repayment.

Small Multifamily Project Guidelines

We are mindful that not every developer has the expertise and capacity to pursue larger-scope projects with more than 20 units. This, however, should not impede them from having the opportunity to start smaller projects that may be a better fit for their current experience level.

Old guideline: stringent requirements on projects under 20 residential units; did not allow developments with less than 10 units

New guideline: Eliminated requirements on projects under 20 residential units and now allow developments with fewer than 10 units

Smaller unit projects often have higher credit risk because a single vacant unit could jeopardize the project’s ability to make loan payments. However, smaller projects are an important stepping stone for many developers trying to build their portfolios, and we can mitigate the risk with other things like operating reserves and technical assistance.

That being said, we do have minimum loan sizes (now $500,000), but this does not have to impede borrowers from coming to us, as we are actively building a partner network to which we can refer clients in need for smaller loan sizes.

Streamlining Lending Approval Processes

As a mission-driven organization, it became all the more important for us to improve efficiencies in lending approval processes so as to be able to serve entrepreneurs and their communities seamlessly.

To that end, we have worked on the follow updates:

Eliminated credit committee approval to be able to issue term sheets to borrowers;

Reduced the size of our credit committee and streamlined approvals for lower-dollar loans;

Moved away from issuing commitment letters upon loan approval, and switched to issuing approval letters that are less of a legal document and more of a summary of terms. The reasoning behind this is that we want to avoid putting borrowers in a position where they have to make legal decisions prior to engaging legal counsel, and we also want to streamline our process to close loans more quickly.

Pivoting to Achieve Financial Equity for Our Communities

The changes above are only a starting point. We are committed to adapting to the needs of our borrowers by adding new products and continuing to evolve our credit guidelines in a way that meets the needs of our borrowers. In addition, we are building out a more robust network of technical assistance for our borrowers that ultimately reduces credit risk to both the borrower and the lender. One great example of that is our EDI program. Through EDI, we aim to provide capacity building in the form of training, mentorship, access to technical assistance, and predevelopment grants (where/when available) to community-centric developers, so as to enable them to succeed in projects appropriate to their levels of expertise.

We are continuing to think through how we can fold equity into our credit guidelines to transform how capital and investments flow into communities. We are excited to share more about our journey as we grow and evolve to serve communities.

Contact us today to start a conversation about how Momentus Capital can support your journey to success.

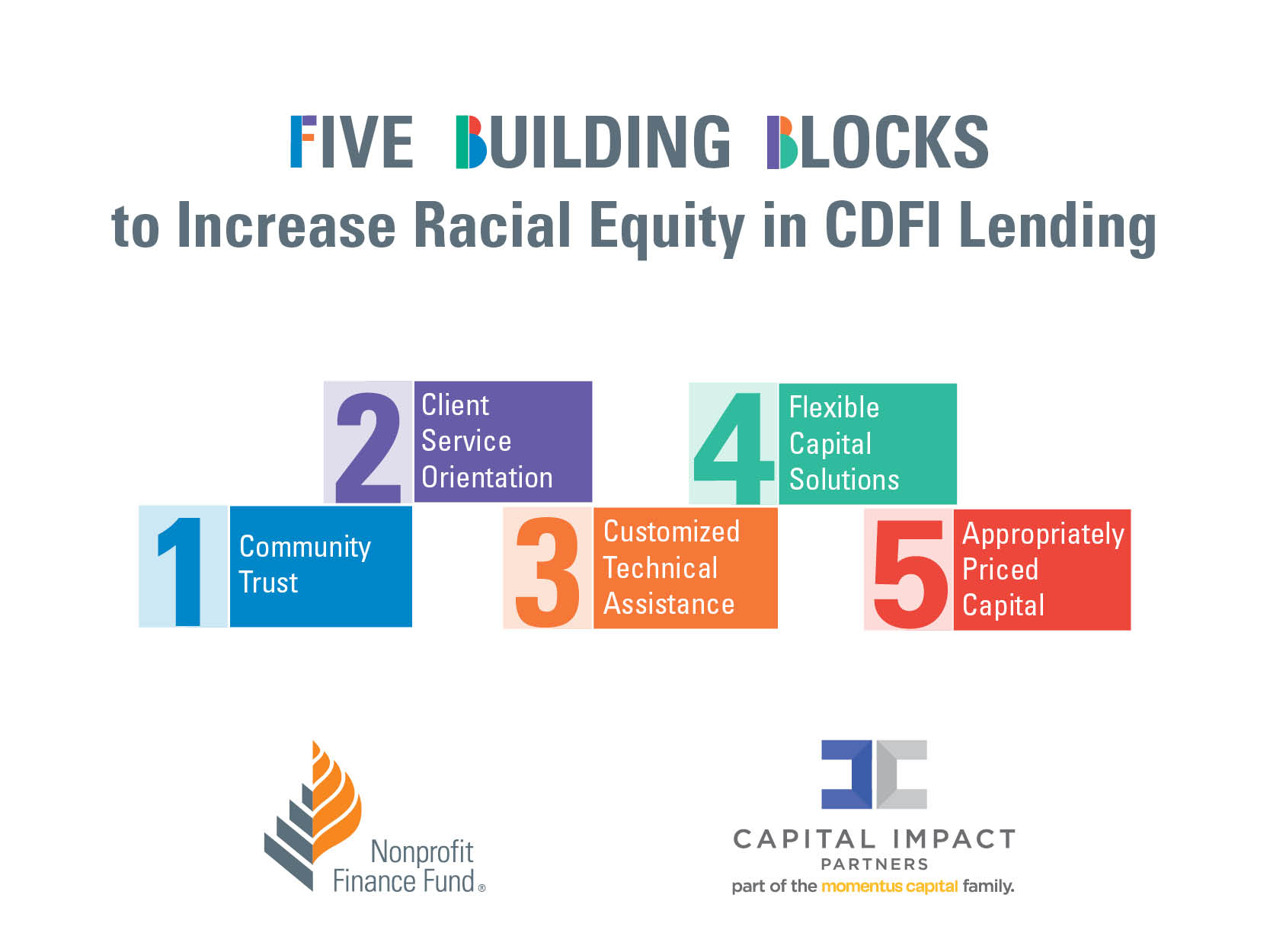

Community Development Financial Institutions (CDFIs) were born out of the civil rights movement to ensure that nonprofits and businesses — particularly those in underestimated communities and communities living with lower incomes — have equitable access to loans. Yet, CDFIs are part of a financial system embedded with discriminatory lending practices which need to collectively be addressed in order to fully achieve the intended goal of equalizing access to financial resources for all people.

Momentus Capital’s family of organizations, including Capital Impact Partners, CDC Small Business Finance, and Momentus Securities, is working to help support economic mobility and wealth creation through more equitable access to capital for communities that have been long overlooked by traditional financial organizations.

In line with this commitment, and in recognition of discriminatory lending practices identified within CDFIs, Capital Impact Partners collaborated with Nonprofit Finance Fund (NFF) to identify and address policies and practices that contribute to it. We conducted research to understand how some local and national CDFIs have successfully taken steps to address inequity within their own lending practices.

As the first quarter of 2023 unfolds, Momentus Capital team members are starting to see trends for an exciting year ahead. And while 2022 proved to be another rollercoaster ride for the economy and small businesses, our experts still forecast plenty of opportunities to make 2023 a groundbreaking year in mission-based lending.

In this year’s predictions, we take a deep dive into a wide range of topics, including how communities can lead the way to greater economic prosperity, how we can get more capital into the hands of small businesses, and potential legislative changes on the horizon. Ultimately, we remain focused on how these factors could impact our borrowers, partners, investors, and the communities we serve. This valuable foresight serves as a compass for existing entrepreneurs and those embarking on their ventures.

Please read the rest of this blog on the Momentus Capital website.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.